New Homes Are More Affordable Now Than They Were in 2016, According to a New Study

每月支付新的,如果家庭cheaper than they were in 2016 in some markets across the U.S., according to a new study. In its report, housing market research firmMeyers Researchexamined adjusted home prices and mortgage rates across 15 markets in the United States, and analyzed data on monthlymortgage paymentsover the past four years. Their research found that in several major markets, home payments are lower as of July 2020 compared to 2016.

For more content like this follow

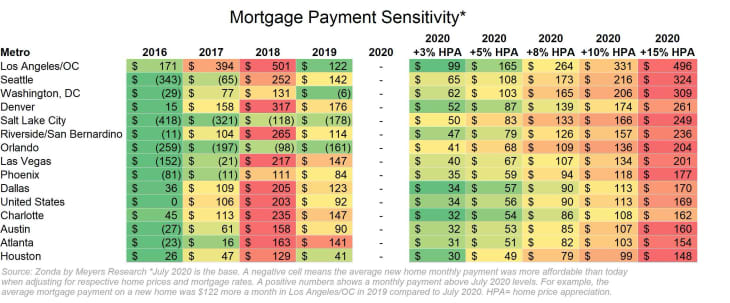

In Los Angeles, payments in 2016 were $171 higher than they are today. Other cities with lower payments on average include Denver ($15 lower compared to four years ago), Dallas ($36 lower), Charlotte ($45), and Houston ($26). In those five markets, monthly mortgage payments were higher in each of the previous four years than they are today. In the United States overall, average payments have seen no change compared to 2016.

Of the 15 markets analyzed, monthly mortgage payments have risen the most compared to 2016 in Salt Lake City, where the average price was $418 less that year than today. Other markets that were more affordable four years ago include Washington, D.C. ($29 less in 2016), Seattle ($343), Riverside/San Bernardino ($11), Orlando ($259), Las Vegas ($152), Phoenix ($81), Austin ($27), and Atlanta ($23).

Compared to 2019, payments are lower today in all of the 15 markets, excluding Washington, D.C. ($6 less in 2019), Salt Lake City ($178), and Orlando ($161). The biggest decrease over last year is in Denver, where the average payment was $176 more in 2019 compared to today.

Although monthly mortgage payments are more affordable in many cities, that doesn’t tell the whole story about the overall affordability of the housing market. Home prices are on the rise, but historically low mortgage rates are helping to mitigate that effect.

“The assumption is that mortgage rates will stay low for the foreseeable future,” says Ali Wolf, chief economist at Meyers Research. “That helps, but doesn’t eliminate, the risk that the housing market could still face an affordability crunch if home prices continue to rise at the rapid pace.”

In other words, we’re not in the clear.

“In particular, if home prices rise 10 percent more than where we are today, consumers will really start to feel pinched and many may become priced out of the market,” she says.

Despite low rates, high home prices coupled with financial insecurity caused by the coronavirus pandemic means that many are putting theirhome buying dreams on holdfor now. However, some buyers that are in a good financial position should consider buying while lending rates remain low, according to realtor Robyn Flint ofTheTruthAboutInsurance.com.

“There are homes listed, but not enough,” Flint says. “It is a seller’s market as indicated by home prices, but it is a great time for buying if you’re equipped. Just be sure to make a strong offer to avoid a bidding war.”