The Key to Buying a Home? Be a White College Graduate, According to This Data

As anyone who’s ever played Monopoly knows, homeownership helps build wealth over time (er, if it doesn’t bankrupt you). It’s not through any kind of financial alchemy or anything. It’s just that, at some point, instead of circling around the board and owing rent everywhere you land, scraping by until you pass Go and collect a paycheck, you’ll eventually own something. Maybe you’ll be the one collecting rent on St. James Place.

这就是为什么a declining overall homeownership ratehas some economists worried about income inequality in the US. And it’s why a newstudyby Apartment List showing a stark racial divide in the homeownership rate is so concerning.

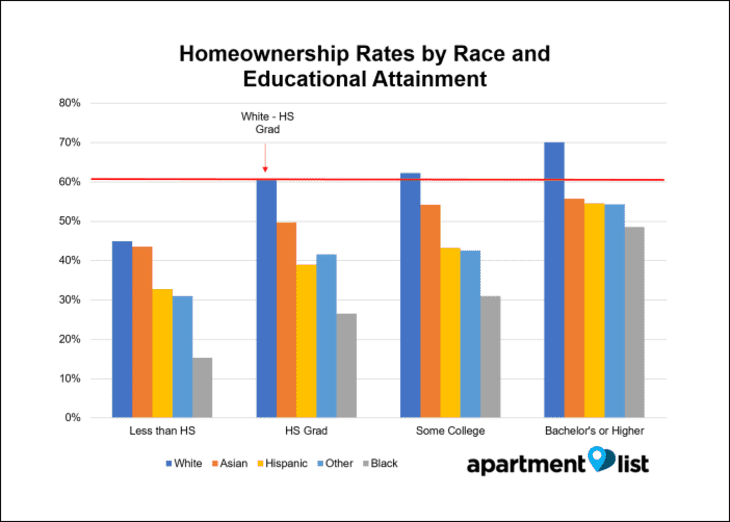

Apartment List studied US Census data for Americans between 25 and 54 years old, and found that while 64.4% of white households were homeowners, that was almost twice the rate of black households (32.7%). Among Hispanics, 41.1% owned their residence, while 54% of Asian households were homeowners.

In general, more diverse cities had smaller racial gaps in the homeownership rate — although in some cities, like Los Angeles and San Francisco, that could be because fewer people of any race can afford a home. But even metro areas where the homeownership gap between white and minority households was smallest — in Miami, San Diego, Jacksonville, Fla., Washington, and Austin, Texas — it was still in the double digits. The highest racial gaps — upwards of 33% — were in northern states like the Dakotas, Montana, Minnesota, and Vermont.

Apartment List found other gaps in homeownership rates as well, including a 15% chasm between college graduates and those with a high school diploma. That’s not too surprising: Homes are expensive, and more and more good-paying jobs now require a college degree. But consider this: White households with just a high school education were still more likely to own a home than college graduates of any minority group.

That’s messed up. There are a lot of reasons for this, some of which go back almost a hundred years — like the US government’s official Depression-eraredlining policiesthat denied minority homebuyers fair financing, and the institutional racism that prevented black Americans from taking full advantage of the post-war G.I. Bill. It’s a sprawling injustice spanning generations: If your grandparents couldn’t buy a house, they’d have had a harder time amassing wealth, and couldn’t pass one down to your parents.

And the problem isgetting worse, not better. The “land of opportunity” is looking more like the “land of staggering income inequality,” with the richest 1%now controlling a record 38.6%of the wealth.

In a nation that’s increasingly diverse — every one of the 50 biggest American metro areas grew less white from 2000 to 2015, according to the study — we need to focus on policy that helps minorities participate in the American dream. “It’s increasingly important to prioritize policies aimed at promoting homeownership among minority and low-income Americans to lessen inequality,” writes Apartment List housing economist Chris Salviati, who recommends increased integration at the neighborhood level and more affordable housing construction. Another step toward advancing housing equality would be to eliminate the mortgage interest deduction — a tax break that, despite its widespread popularity,mainly benefits wealthy homeowners to the tune of $71 billion a year.

Now, you’d think that if most American homeowners are white, they’d have been the hardest hit when home values plummeted during the housing crisis, right? I mean, if ever there was a good time not to be a homeowner, it was from 2007 to 2009. And yet, the recession dramaticallyworsened the wealth gapin America, as minoritieslost more home equityfrom 2005 to 2011 than white homeowners.

我怀疑更深层次的经济将支撑这些numbers. For example, during an economic growth cycle, it usually takes longer for employment and wage gains to reach low- and middle-income households. That might mean they’re not able to afford a home until three or four years into a boom cycle — after the property market has already gone up in price (and is that much closer to the next crash).

A recent Federal Reserve study illustrates just that. African American and Hispanic households saw thefastest gains in household wealthfrom 2013 to 2016, at 30% and 46%, respectively. That’s welcome news, though it’s largely because minority households were starting from so far behind. “If you go from having very little to doubling that, you still may not have very much but you see a big percentage gain,” Jeffrey Eisenachtold the Washington Post.

Meanwhile, the lag of the economic growth cycle is clear: White households were the only racial group to see their incomes increase from 2010 to 2013… which would have been precisely the best time to buy a home. By 2013, the current upward march in home prices was already well underway — just as minority households were finally starting to see some better income growth.

America’s economic racial divide is a problem that goes far deeper than just housing, and policies that encourage minority homeownership can only do so much. But we’ve got to start somewhere.